Deep dive into the Chinese AM industry – learn the funding amounts for companies in 2024

The Atomic Layers: S7E21 (00199)

Atomic Layer of the Day:

Somehow this week has turned into one dominated by China’s 3D printing industry. Even when I write about something else, its presence lingers over my keyboard.

Today, we're talking about China again—this time, its domestic market.

The 3DPrint.com portal came across an interesting report on the Nanjixiong platform, and thanks to the generosity of Chinese AI, DeepSeek, I translated it into my native language. (Just to be sure, I double-checked it using old-school Google Translate).

The article covers investments made in the 3D printing sector in recent years. It turns out that last year, this sector experienced a sudden collapse. However, if you exclude the two largest investments of 2023, the downturn actually began two years ago…

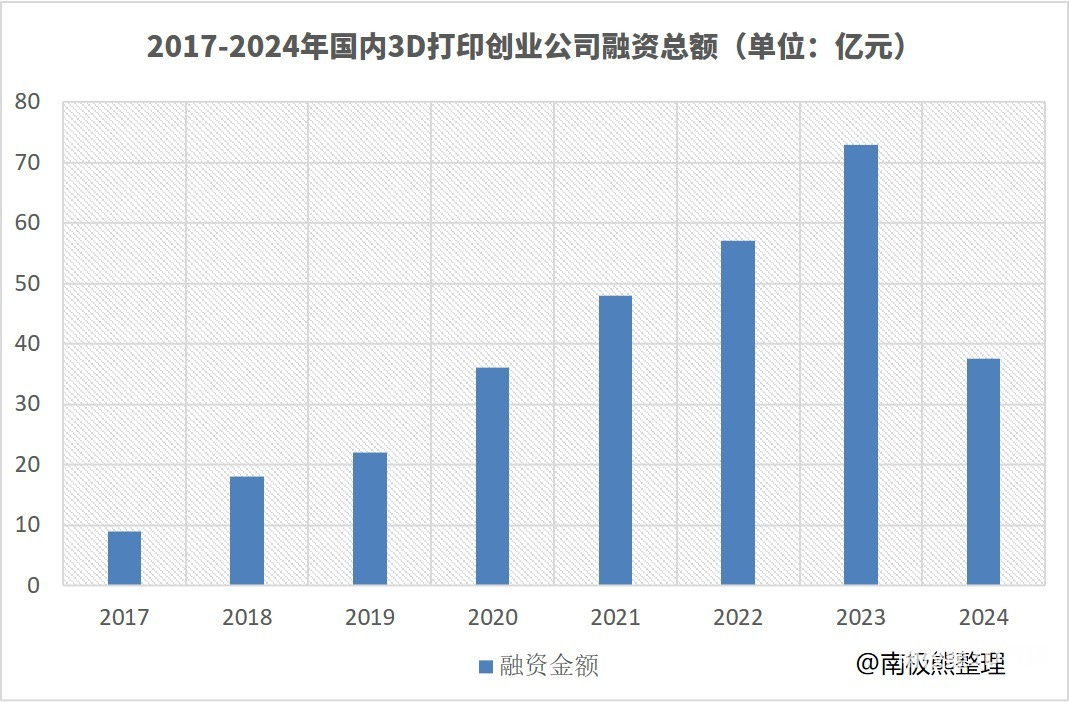

Let’s start with this chart:

According to Nanjixiong, there was already a significant decline in 2023, but it was masked by two major funding rounds. Polylite completed a private public offering worth over 3 billion yuan, while Farsoon High-Tech successfully went public on the Science and Technology Innovation Board, raising 1.105 billion yuan. These two investments accounted for 56% of the total industry funding.

Does this mean that China's 3D printing industry is going through the same nightmare as the American and European markets? Yes and no…

According to Nanjixiong, between 2017 and 2023, China’s 3D printing industry experienced impressive investment growth, with annual funding increasing from 900 million to 7.3 billion yuan (approximately $125 million to $1 billion).

In 2024, there was a significant decline in investments, which can be attributed to both internal and external economic factors. The year saw 32 investment cases in the 3D printing sector, totaling about 3.75 billion yuan (~$510 million), marking a 49% decrease compared to the previous year.

However, this decline does not indicate a lack of interest in 3D printing technology but rather reflects broader trends in the capital market.

Since August 2023, when China’s Financial Supervision Commission announced a "phased tightening of IPO approvals", the capital market has undergone significant changes. In 2024, only 94 companies successfully went public, a 69.97% drop compared to the previous year. This shift also affected the 3D printing sector, forcing many companies to slow down their IPO preparations.

Despite these challenges, China’s 3D printing industry continues to grow, with the domestic market reaching a value of 50 billion yuan (~$6.9 billion) in 2024.

Among the funded companies, 3D printer manufacturers dominate. Below I listed just a few of them. Get ready for a list of names that probably won’t mean much to you…

Metal AM systems:

Hanbang Technology secured Series B funding in February 2024 and Eplus3D received Series B+ funding in July 2024; both raised “several hundred million yuan”

Rongsui Technology, specializing in DED technology, raised tens of millions of yuan in a Pre-A+ round in May 2024.

3D printing materials:

Weilai 3D raised 260 million yuan in Series B funding (February 2024)

Shangcai 3D secured nearly 100 million yuan in Series A & A+ funding (August 2024)

Dingyi Technology raised an undisclosed amount in Series B (July 2024).

Polymer 3D printers:

Yingpu 3D, known for SLS technology, secured Series A funding in February 2024 (undisclosed amount)

Huasheng Composite secured “tens of millions of yuan” in Series B (December 2024)

Anaiso 3D received nearly 100 million yuan in Series A funding.

3D Printing services:

Yuding Additive secured “several hundred million yuan” in a strategic funding round (April 2024)

Yingwei Medical raised 20 million yuan in Series A+ (March 2024).

According to the article’s authors, although 2024 saw a sharp drop in 3D printing investments in China, this reflects general market conditions rather than a decline in interest in the technology.

This information is extremely valuable because, despite year-over-year declines, investments are still happening—and they involve companies completely unknown in the West.

This only highlights the immense potential of China’s 3D printing industry, which we might not even be fully aware of…

Atomic Layer from the Past:

02-21-2022: 9T Labs received multi-million dollar funding from Stratasys and Solvay.

GET FREE HISTORY BOOK: ‘2012 in AM’

News & Gossip:

Protolabs published report for 2024. The company reported total revenue of $500.9 million. The 3D printing sector experienced a slight decline, totaling $83.8M in 2024, down from $84.3M in 2023. This means, that 3D printing is responsible for just 16,7% of revenues, yet the company is still listed on various lists and comparision tables as AM related.

Tethon 3D acquired TA&T from Sintx to strengthen its position in ceramic additive manufacturing. The deal enhances Tethon’s manufacturing capabilities, expands its resin portfolio, and boosts global market reach.

And now a sneak peek of my article tomorrow. Autodesk shows no signs of slowing down and equips Fusion with another major 3D printing feature! Yes, my friends, Fusion now includes a slicer for Bambu Lab printers (X1, X1C, X1E, P1P, P1S), allowing direct G-code generation. AMS - multiple color and material support is not yet available.

Is there a historical dataset to show the seed and investor rounds in the bigwigs like Polymaker,Elegoo etc