Seems like AM is back in line

3DP War Journal #71

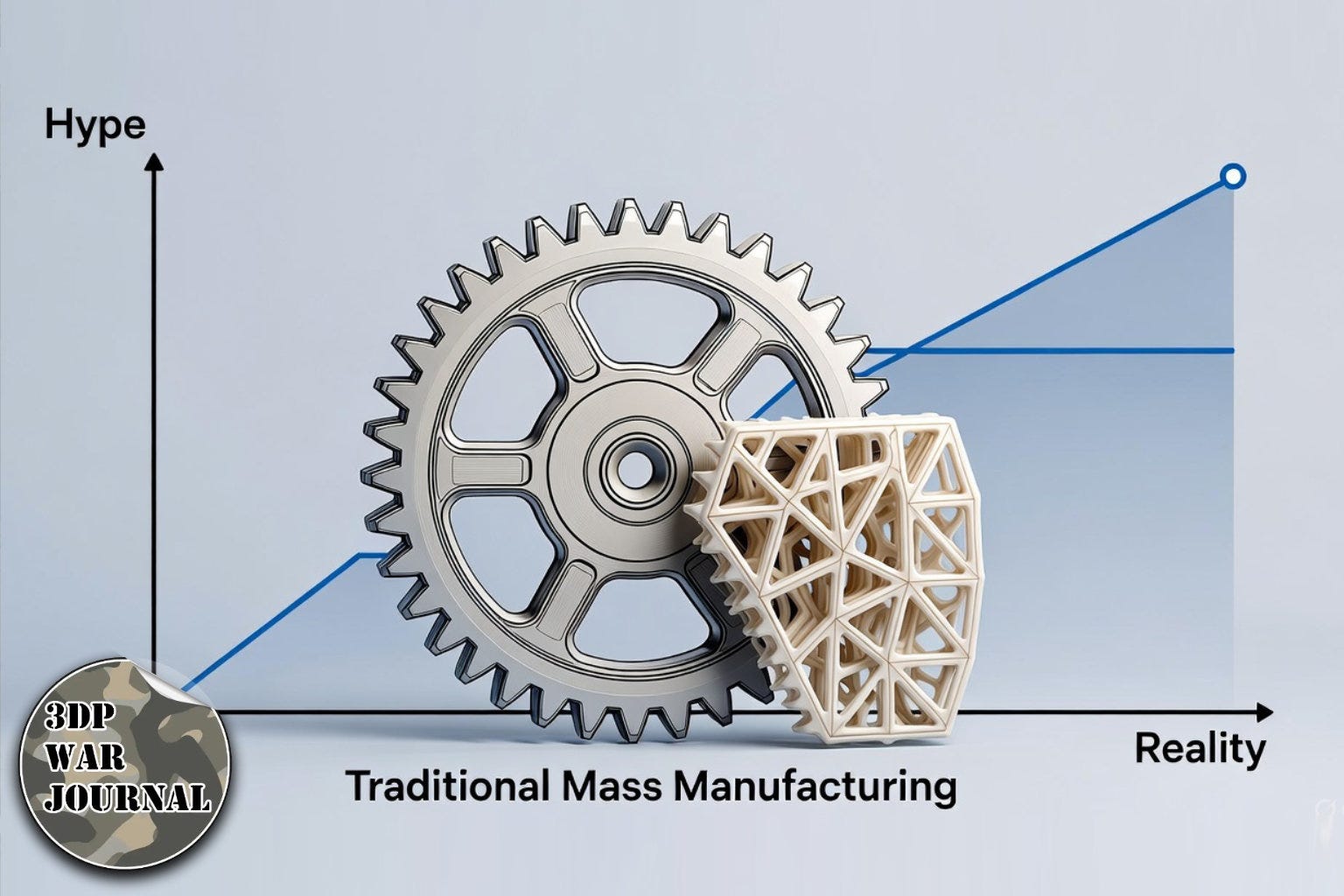

After a period of immense enthusiasm within the industrial manufacturing community, 3D printing technology has entered a phase of correction. It is no longer seen as the vanguard of a “new industrial revolution,” but has instead assumed a much more balanced role.

One could say that AM is finding its proper place in the hierarchy - it remains useful, but without trying to dominate the entire production chain.

3D printing is not disappearing; however, its share and significance in full-scale industrial production are being rationalized.

This thesis is well illustrated by the latest financial results of Protolabs and Xometry - two global platforms operating within the digital, on-demand manufacturing model. In the first case, while the company as a whole continues to grow, its 3D printing segment not only failed to expand but actually declined. In the case of Xometry, the available data do not separate revenues derived from 3D printing - which in itself may suggest that this area is treated more as one component of a much broader offering.

This should come as no surprise, since it perfectly aligns with the II Market Law of Additive Manufacturing: „a successful company in the 3D printing industry will always be smaller and less profitable than a successful company in another industrial sector.”

From hype to reality

3D printing as a technology has become well established - customers now understand when it makes sense to use it and when it does not. Yet even at the peak of industry enthusiasm, there was already an awareness that it would not replace mass production in sectors demanding high repeatability, low unit costs, and extreme efficiency.

From that perspective, the latest data from Protolabs and Xometry confirm that 3D printing has found its place: it remains valuable and relevant, but by no means dominant.

Looking at the details: in the third quarter of 2025, Protolabs achieved record revenue of $135.4 million, an increase of roughly 7.8% year over year. Net income totaled $7.2 million, roughly matching last year’s figure.

The strongest-performing segments were CNC machining (up about 17-18%) and sheet metal fabrication (up about 14%). The 3D printing segment, meanwhile, saw its revenue decline from $21.4 million in Q3 2024 to $20.1 million in Q3 2025 - a drop of about 6.3%.

Xometry, on the other hand, also reported an excellent quarter. In Q3 2025, the company recorded revenue of $180.7 million, up roughly 28% year over year. The “marketplace” division - the company’s core business - generated $166.6 million, a 31% year-over-year increase.

What’s important here is that Xometry does not provide a separate breakdown of revenue derived specifically from 3D printing. The company lists additive manufacturing as one of several production technologies available on its platform - alongside CNC, injection molding, and sheet metal - but does not indicate how much of its income comes from AM.

Therefore, although 3D printing is explicitly mentioned and clearly contributes to growth, it is impossible to determine precisely what portion of revenue it represents. In practice, it can be assumed that its share is not dominant, given that the company’s focus is on the entire spectrum of manufacturing services.

Comparing both companies reveals a clear pattern: 3D printing serves as an important component within a broader portfolio, but it is no longer the main driver of growth.

In ProtoLabs’ case, the decline in its 3D printing segment suggests that customers are increasingly turning to other methods when they need lower unit costs and higher production volumes. In Xometry’s case, although growth is strong, the absence of separate AM reporting suggests that 3D printing is not the company’s primary engine of expansion.

Everything according to plan…

This observation aligns perfectly with the II Market Law of Additive Manufacturing: ”a company focused on 3D printing will always be smaller and less profitable than an equally successful firm engaged in traditional mass production.“

In other words, even when the technology is mature and its applications are proven, economically it remains part of the wider manufacturing ecosystem rather than its dominant force. This does not signal regression or failure for 3D printing - quite the opposite: it represents a more mature understanding and a realistic valuation of its role.

There are also several broader conclusions to draw:

First, companies that offer 3D printing as one of many manufacturing processes (such as CNC, molding, or sheet metal) tend to perform better than those built exclusively around additive manufacturing. Protolabs and Xometry exemplify this approach.

Second, customers are increasingly interested in short-run production and the flexibility it brings - areas where 3D printing truly shines. However, when it comes to large-scale production, lower unit costs, and economies of scale, traditional methods still hold the upper hand.

Third, amid global macroeconomic uncertainty, industrial clients are inclined to choose more “proven” technologies - which may also explain why Protolabs’ 3D printing business weakened in Europe.

Overall, 3D printing technology is moving from a phase of hype and spectacular promises to a more measured, stable mode of operation. In light of the II Market Law of Additive Manufacturing, this evolution is logical and expected: the success of 3D printing does not imply dominance over traditional technologies, but coexistence and complementarity.

#7. 3D Systems published financial report for Q3 2025

3D Systems reported Q3 revenue of $91.2 million, down -19% from $112.9 million a year earlier. Despite this decline, the company sees hopeful signs as key markets like healthcare and aerospace show early recovery. The net loss significantly improved to $18.1 million, aided by major cost-cutting. CEO Jeffrey Graves noted customer spending is picking up. Management forecasts an 8-10% sequential revenue increase for Q4, driven by new product launches and a typical year-end boost in client spending.

READ MORE: www.3dprint.com

#6. AMAZEMET automated metal powder production with AI

AMAZEMET has integrated an AI model into its rePOWDER platform, aiming for largely unsupervised ultrasonic atomization in powder production. This addresses a key bottleneck in labs, where metallurgical processes often require constant operator attention. The AI uses machine vision, analyzing a live stream of the melt pool to automatically control the torch, wire feed, and ultrasonic parameters. This ensures stable operation for high yields of the desired particle size distribution. The system can reportedly run unsupervised for at least four hours, with a goal of eight.

READ MORE: www.3druck.com

#5. XJet launched new compact Carmel Pro 3D printer

XJet has launched the Carmel Pro, a new compact metal and ceramic 3D printer designed to democratize access to its technology. The new model is significantly smaller, over 75% lighter, and boasts a 60-70% lower cost-of-ownership than its predecessors. XJet plans to start shipping the Carmel Pro in the second quarter of next year, positioning it as a key tool for innovators and the reshoring ecosystem.

READ MORE: www.3dprint.com

#4. Reinforce3D installed CFIP system at spanish manufacturer

Reinforce3D is advancing the industrialization of its Continuous Fiber Injection Process (CFIP) with a new DELTA system installed at Spanish contract manufacturer Pantur. The CFIP technology strengthens 3D-printed polymer parts by injecting continuous fibers into predefined hollow channels post-printing. This automated process enhances rigidity and durability without altering the component’s external geometry.

READ MORE: www.3druck.com

#3. Hanwha Defense USA Invested in Firehawk Aerospace

Hanwha Defense USA has made a strategic investment in Firehawk Aerospace, a Dallas-based company specializing in rocket propulsion. The partnership will focus on advancing solid rocket motor technology and production, leveraging Firehawk’s expertise in additive manufacturing. This investment aims to accelerate the full-rate production of 3D-printed propellant and the development of integrated missile systems.

READ MORE: www.voxelmatters.com

#2. Replique expanded into Southern Europe with new italian subsidiary

Replique, a provider of an on-demand industrial production platform, has established a new subsidiary in Milan, Italy. This strategic move aims to strengthen the company’s presence in Southern Europe and operate closer to its customers. The expansion will allow Replique to better tailor its digital manufacturing services—including 3D printing, CNC machining, and injection molding—to regional requirements. The company reports that series production is a key growth driver, with the average order quantity now around 100 parts, five times higher than the previous year. Replique’s global network encompasses over 350 qualified manufacturing partners.

READ MORE: www.3druck.com

#1. Angstrom Group acquired Mantle

Angstrom Group has acquired Mantle, a metal additive manufacturing startup. This move aims to accelerate advanced manufacturing capabilities across Angstrom’s global operations. Mantle’s TrueShape technology integrates metal 3D printing with CNC machining to produce precision tooling components for injection molding, offering a faster and more cost-effective alternative to traditional methods. As a Tier 1 automotive supplier, Angstrom plans to scale this technology across its 41 production facilities worldwide.

READ MORE: www.voxelmatters.com

Great article. Agree that reevaluation of the industry has taken place over all. But within some print technologies with less steps or leaner procedures the possibility of producing industrial components and consumer goods is still possible with correct support technologies in post-processing to achieve compliance needs. Just need to think-outside-the-box