Stuck in stagnation

3DP War Journal #59

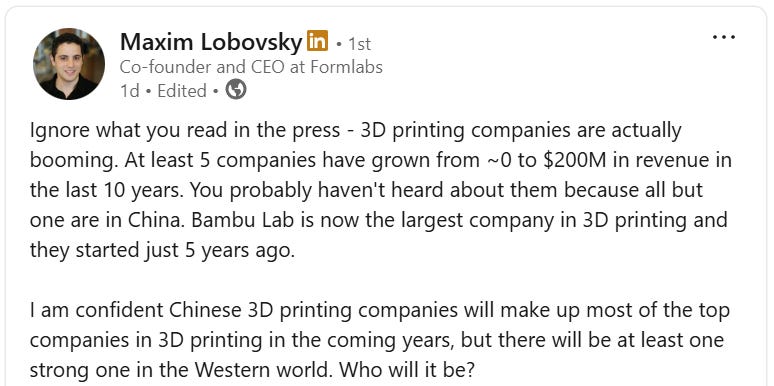

Last week, Maxim Lobovsky wrote two things – one on LinkedIn:

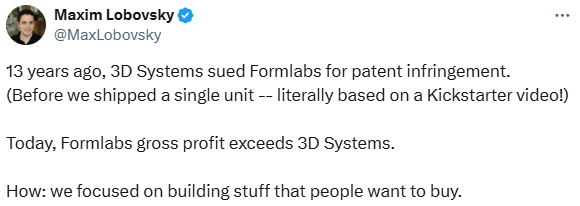

and another on X:

I don’t know to what extent this was coincidental and to what extent deliberate timing, but both posts happened to appear in the very same week that 3D Systems released its Q2 2025 financial results.

Stratasys did the same, so I decided to take a closer look at both companies, reflect for a moment on their performance, and share some thoughts. Here they are…

3D Systems and a decade of slowing down

In Q2 2025 the company reported revenue of $94.8 million, a decline of -16% year-over-year. However, on a sequential basis revenues actually grew by about +8% – if we exclude sales from the divested Geomagic business, which was sold at the very beginning of the quarter.

Structurally, the Healthcare segment saw revenues decline -8% YoY to $45.0 million, while Industrial Solutions fell -23% to $49.8 million. The only real bright spot was Aerospace & Defense, which grew by +84% YoY and +53% QoQ.

Gross margin fell from 41.6% to 38.1%, while the non-GAAP gross margin came in at 39.2% (versus 40.9% a year earlier) – a decline attributed to changes in the revenue mix following the sale of Geomagic.

Crucially, the company posted net income of $104.4 million, reversing a loss of -$27.3 million in Q2 2024 – an increase of +482%. However, it must be emphasized that this result was driven primarily by one-off events: gains from the sale of Geomagic and debt extinguishment.

Adjusted EBITDA was still a loss of -5.3 million USD, albeit an improvement of $7.6 million year-over-year.

In terms of liquidity, the company had $133.9 million in cash and restricted cash, against net debt of $122.6 million. In the first half of the year there was significant cash outflow: operations consumed $59.6 million.

Over the past few years, 3D Systems has been on a declining revenue trend. Annual sales dropped from around $610 million in 2021 to about $440 million in 2024 – a decline of roughly 27% in just three years.

Looking further back, from 2010 to the mid-2010s the company grew dynamically, but since around 2014 it has suffered a clear regression. Operational cash flows have remained negative – a sign of long-lasting liquidity challenges.

What does all this mean? Is 3D Systems “withering”?

In my view, the situation at 3D Systems is more complex than a simple “growing” versus “dying” dichotomy.

Despite all the negative developments, especially the steadily shrinking top line, the return to positive net income is a positive milestone – even if it is largely one-off. From an efficiency perspective, cost reductions are generating savings of over $20 million per quarter. The balance sheet restructuring (debt extinguishment, extended maturities, share buybacks) is improving financial stability. The noticeable growth in key sectors (A&D, medtech) provides signs of strategic redirection and partial revival – particularly in areas of higher added value.

On the other hand, fundamental weaknesses persist. Revenues are still declining, mainly in Healthcare and Industrial. Gross margins are falling, and operating income (adjusted for extraordinary events) remains negative. Operating cash flow continues to be in deficit, underscoring the need for further restructuring. The path to sustainable profitability is still bumpy.

It seems clear by now: 3D Systems will never again become the company it was expected to be in the mid-2010s (at least according to Avi Reichental’s vision).

It has been reduced to a kind of historical leader, maintaining its position largely thanks to legacy implementations and contracts.

3D Systems still carries the reputation of being “big and innovative,” but that perception is increasingly challenged as new and existing customers take a closer look at what competitors have to offer…

Stratasys and the flattening of a flat trend

Unlike 3D Systems, which is seeing declining revenues, Stratasys posted Q2 2025 revenues of $138.1 million, essentially flat compared to the same period in 2024 ($138.0 million). The company emphasizes that its business model is resilient thanks to recurring revenue from services and materials, which cushion the volatility in new 3D printer sales.

Gross margin declined from 43.8% to 43.1% GAAP, and from 49.0% to 47.7% non-GAAP. This reflects mild cost pressure, though margins remain well above 3D Systems’ levels (around 38–39%).

More importantly, operating performance improved: GAAP operating loss narrowed to -16.6 million USD (from -26.0 million a year earlier), while on a non-GAAP basis the company posted a small operating profit of 1.1 million USD, compared to a loss in 2024. This is a breakthrough signal, pointing to improved efficiency.

At the bottom line, Stratasys still reported a GAAP net loss of -16.7 million USD, but in non-GAAP terms delivered a net profit of 2.2 million USD. Adjusted EBITDA reached 6.1 million USD, more than double the prior year (2.3 million USD).

Operating cash flow was slightly negative at -1.1 million USD, but still better than last year (-2.4 million USD). The company’s strongest asset is its balance sheet: $254.6 million in cash and no debt. This places Stratasys in a far stronger financial position than 3D Systems, which struggles with debt service costs and negative cash flows.

The company updated its full-year 2025 guidance, projecting revenues of $550–560 million, which would represent moderate growth over 2024 (~$536 million). It expects results to improve in the second half of the year, especially in Q4, when EBITDA is forecasted to reach at least 8% of revenues. For the full year, Stratasys anticipates non-GAAP net income of $11–13 million, a meaningful reversal from historical losses. On a GAAP basis, however, a net loss of -66 to -77 million USD is still expected.

From a long-term perspective, Stratasys has followed a trajectory similar to 3D Systems: rapid growth in 2012–2014 fueled by the 3D printing boom, followed by a long stagnation and declining revenues. In 2014, revenues topped $750 million, whereas today they are lower by about 25–30%.

In other words, the company has not regained the scale it once had. Yet unlike 3D Systems, which has shrunk to under $0.5 billion in annual revenues, Stratasys has managed to hold steady around the $0.55 billion mark. The past few years (2021–2025) reflect stagnation, but not collapse.

It is also worth noting that Stratasys has maintained a conservative balance sheet for years, practically debt-free, which shields it in times of market stress. Unlike 3D Systems, whose share price has fallen to around $2, Stratasys stock—though far below past highs—remains above “technical death” levels.

At present, Stratasys presents itself as a stable and relatively healthy company, albeit with low growth.

Still, it is difficult to call it a “growth company.”

For more than a decade, its revenues have been essentially flat or slowly declining.

Stratasys appears more like a company that is enduring—keeping afloat, resilient to market swings, but not showing signs of entering a growth phase.

Back to Formlabs

Although, as Max pointed out on LinkedIn, Bambu Lab is today the world’s largest 3D printer manufacturer, Formlabs is the true outlier in the AM market.

Founded in late 2011 at the very beginning of the consumer 3D printing boom, Formlabs quickly became one of its leaders. The culmination of that era was Maxim Lobovsky’s appearance in the famous Netflix documentary Print the Legend.

When the consumer 3D printing wave subsided, Formlabs—unlike most of its peers from that generation—successfully reinvented itself as a provider of professional solutions for both industrial and medical markets.

It then expanded into a second AM technology beyond SLA—SLS—and rapidly became a market leader (at least in terms of installed systems).

Formlabs went on to be one of the leaders of the third era of the AM market—Mass Additive Manufacturing—which has only recently come to an end.

Yet the company has emerged from this period untouched by the downturn it caused. Quite the opposite—just as Max highlighted, Formlabs has now, for the first time ever, overtaken 3D Systems.

The very company that, at Formlabs’ birth, tried to litigate it out of existence.

I wrote last year about why Formlabs is different. Today it’s even clearer: the company is not slowing down and keep growing.

Unlike the old, legacy players that got stuck in stagnation...

#7. Swiss Steel Group and Ugitech launch UGIWAM wire for AM

Swiss Steel Group and its subsidiary Ugitech (France) have introduced UGIWAM wire, a breakthrough for Wire Arc Additive Manufacturing (WAAM). This solution enables precise component production with custom alloys tailored to industry needs. As the only European filler metal producer with its own steel mill, Ugitech controls the wire’s chemical composition, ensuring high customization. The wire’s performance is enhanced by R&D, optimizing deposition and weldability. Ugitech also focuses on decarbonization, providing CO₂ footprint data for each product.

READ MORE: www.voxelmatters.com

#6. ASTM International developed new standard for metal AM powder contamination detection

ASTM International’s additive manufacturing committee is drafting a new standard (WK80171) to guide detection, quantification, and classification of contamination in metal AM powder feedstock. Developed by subcommittee F42.01, the standard will help powder manufacturers and laser beam powder bed fusion (LB-PBF) users.

It will define contamination types, outline detection methods (e.g., optical microscopy, SEM, X-ray CT, XRF), and detail implementation strategies. The goal is to ensure powder quality and process reliability in metal AM.

READ MORE: www.tctmagazine.com

#5. KCL and CEAD partnered to advance sustainable Large-Format 3D Printing

KCL, a piloting service provider, has partnered with CEAD, a large-format AM (LFAM) specialist, to expand material options for industrial 3D printing. The collaboration confirms compatibility between CEAD’s hybrid systems and KCL Formi, a high-performance biocomposite made from cellulose pulp fibers instead of traditional carbon or glass fibers.

READ MORE: www.voxelmatters.com

#4. Bambu Lab partnered with Helio Additive to bring industrial-grade simulation to desktop 3D printing

Bambu Lab has teamed up with Helio Additive to integrate Dragon, an advanced thermal simulation engine, directly into BambuStudio. This enables users of X- and H-series printers to optimize prints by predicting heat distribution, layer adhesion issues, and deformation risks before printing.

The voxel-based system provides a Thermal Index overlay with optimization tips, reducing failed prints and material waste. Initial tests show improved strength, less warping, and faster print speeds.

READ MORE: www.3dprintingjournal.com

#3. FibreSeeker 3 brings industrial-grade carbon fiber 3D printing to desktops

The FibreSeeker 3 introduces continuous carbon fiber 3D printing to desktop users, a technology previously limited to expensive industrial systems. Unlike chopped-fiber filaments, it embeds full-length carbon strands into prints, achieving 900 MPa tensile strength—enough to replace metal parts in some applications.

Using dual extrusion (polymer + fiber), it offers three modes: polymer-only, hybrid, or high-fiber reinforcement. Features include auto-calibration, enclosed build chamber, and AI-assisted print monitoring.

READ MORE: www.3druck.com

#2. Bambu Lab launches enterprise-grade H2D Pro 3D printer

Bambu Lab has unveiled the H2D Pro, an enterprise-ready version of its H2D printer featuring enhanced network security and fleet management support. Priced at $3,799 (including AMS 2 Pro & AMS HT), it adds WPA2-Enterprise Wi-Fi, Ethernet, physical kill switches, and a removable network module for air-gapped security.

The printer supports 802.1X authentication for corporate IT integration and offers custom fleet management software development. Hardware remains identical to the standard H2D, with Toolhead Enhanced Cooling Fan and Tungsten Carbide Nozzle compatibility (available Q4 2025).

READ MORE: www.all3dp.com

#1. Anzu Partners affiliate to acquire EnvisionTec following court approval

An Anzu Partners affiliate has received U.S. court approval to acquire EnvisionTec GmbH, following last week's clearance to purchase ExOne GmbH and ExOne KK from bankrupt Desktop Metal. The deal faces no objections and will proceed immediately.

EnvisionTec, acquired by Desktop Metal in 2021 for $300M, pioneered resin-based 3D printing for dental, jewelry, and automotive sectors. Anzu pledges business continuity, honoring existing contracts and partnerships. Concurrently, Anzu is also acquiring voxeljet under German restructuring laws. Leadership for EnvisionTec remains unannounced.

READ MORE: www.tctmagazine.com